Posted on: April 23rd 2026

Community banks are operating under sustained pressure, with tight margins, rising compliance costs, and increasing competition from fintechs and large institutions.

Recent industry data reinforces this reality. In the 2025 CSBS Annual Survey, bankers ranked net interest margins as their top external risk, alongside deposit growth, technology costs, and cost of funds. At the same time, FDIC data shows community bank net interest margins at 3.46% in Q1 2025, which is still below the pre-pandemic average of 3.63%.

These pressures directly affect profitability and the ability to grow.

Meanwhile, expectations have shifted:

- Customers expect faster lending decisions

- Regulators expect stronger, real-time oversight

- Competitors are operating with AI & data-driven precision

Most community banks already have the data to respond across core systems, lending, transactions, and customer interactions. But that data is not translating into timely decisions.

The result is not just inefficiency, it is lost revenue, missed growth, and higher risk exposure.

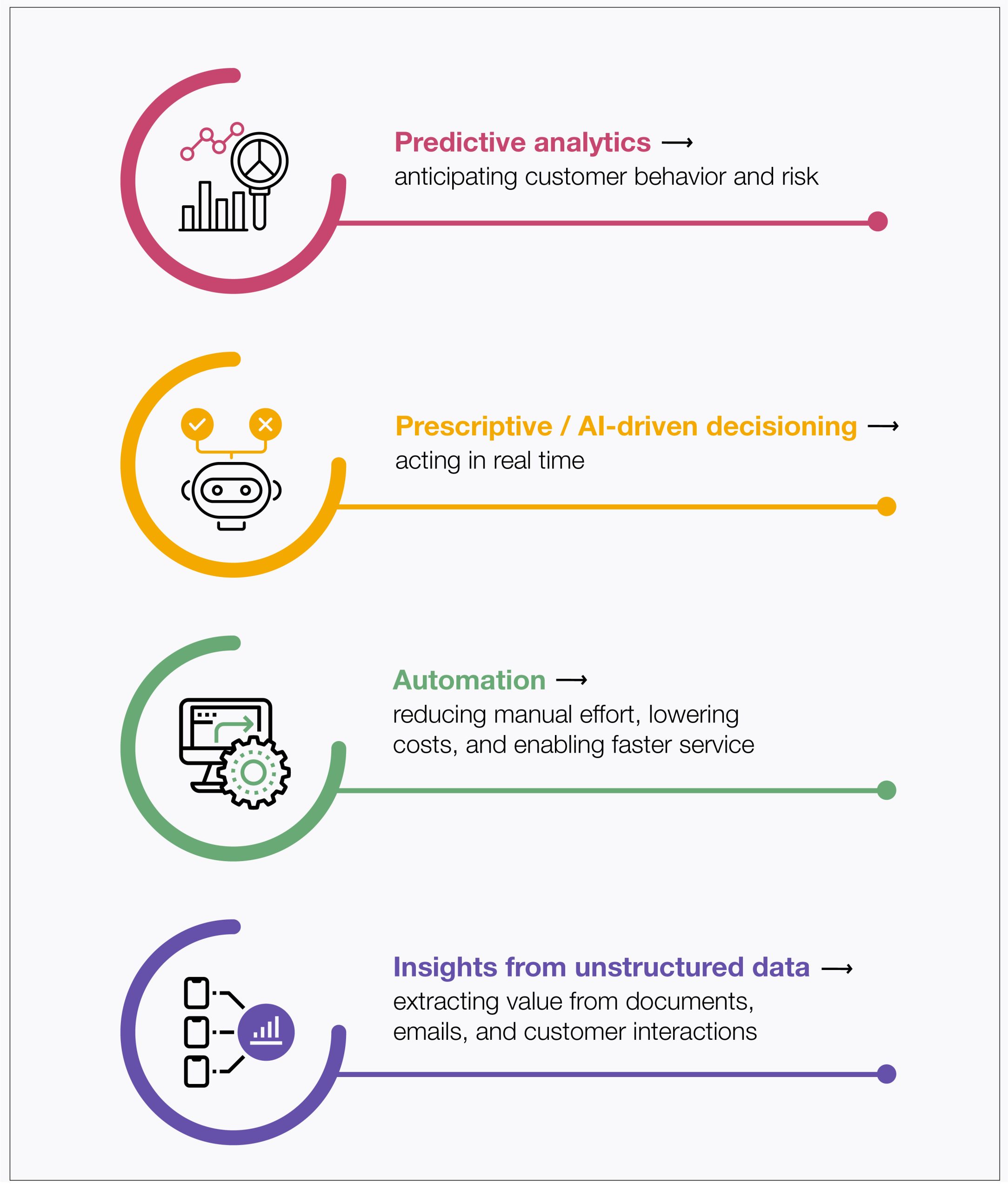

The Analytics Gap Community Banks Face

Most community banks are still operating at descriptive analytics: reports and dashboards that explain what has already happened.

But competitive advantage now lies in:

This gap exists due to structural constraints:

- Fragmented data across core, LOS, CRM, and compliance systems

- Legacy platforms are not built for real-time analytics

- Limited in-house data and AI expertise

- Perceived cost and complexity of transformation

The result: insights remain static, decisions remain manual, and service becomes slower.

The Cost of Inaction

What used to be an operational issue is now a competitive gap.

Loan delays = lost deals

Customers increasingly choose lenders based on speed. Delayed approvals directly impact conversion and revenue capture.

Weak segmentation = lower wallet share

Without behavioral insights, banks cannot identify high-value customers or growth-ready small businesses. This not only limits cross-sell and upsell opportunities but also leads to ineffective, broad-based marketing efforts—driving up acquisition costs while delivering lower returns.

Reactive fraud management = higher losses

Fraud remains a material concern. According to 2025 CSBS findings, card fraud remains the most common and highest-loss category for banks, followed by check fraud.

Banks that are not using data effectively are falling behind those that can act on insights quickly.

Where Analytics Delivers Immediate Value

The opportunity lies in targeted, high-impact use cases, not large transformation programs.

Fraud Detection (Speed + Loss Reduction)

Modern fraud analytics uses transaction-level behavioral models:

- Location, device, and transaction velocity

- Merchant patterns and historical behavior

Deviations trigger real-time alerts, enabling sub-second intervention and faster investigation.

AI-driven fraud operations have demonstrated the ability to continuously detect, investigate, and prevent fraud at scale, significantly reducing loss exposure and improving response times.

Customer Analytics (Growth + Retention)

By combining transaction data, product usage, and engagement signals, banks can:

- Identify high-value and at-risk customers

- Predict churn

- Drive targeted cross-sell

This shifts growth from broad campaigns to precision targeting, improving conversion and customer lifetime value.

Credit Risk & Lending (Speed + Accuracy)

Advanced credit models incorporate:

- Cash flow and transaction data

- Behavioral signals

- Alternative data sources

This enables:

- Faster underwriting decisions

- Better risk differentiation

- Improved approval quality

For community banks, this directly translates to shorter turnaround times and higher win rates in competitive lending scenarios.

P&L Analytics (Visibility + Control)

Linking customer, product, and operational data enables:

- Clear visibility into margin drivers

- Cost-to-serve insights

- Branch and portfolio performance tracking

In a margin-constrained environment, this turns P&L into a forward-looking decision tool, not just a reporting output.

How to Fix It: A Practical Approach

Community banks do not need a massive transformation to get started. A focused, phased approach delivers better results.

- Start with 2–3 high-impact use cases

Prioritize areas like fraud, customer segmentation, or credit risk where ROI is clear and measurable.

- Create a unified data layer

Build a centralized data foundation to integrate key systems and establish a single source of truth.

- Leverage AI to accelerate development

AI can significantly reduce the time required to build, deploy, and scale analytics use cases, from automating data preparation to enabling faster model development and real-time insights. This allows banks to move from insight generation to action much more quickly.

- Leverage external expertise

Partnering with analytics specialists helps overcome talent gaps and accelerates implementation without heavy upfront investment.

- Scale through iteration

Move from reporting to predictive analytics and eventually AI-driven decisioning, expanding use cases as capabilities mature.

The goal is not perfection from day one, but consistent, scalable progress.

Why Straive?

To address fragmented data, legacy constraints, and limited in-house expertise, community banks need more than tools; they need execution. Straive delivers this through:

Conclusion

Community banks already have a lot of data, but using it quickly and consistently is still a challenge. If analytics is treated as optional, decisions stay slow, visibility stays limited, and opportunities get missed. Banks that start using data in their daily decisions, step by step, will move faster, make better decisions, and grow more profitably.

At the end of the day, what really matters is how well and how quickly a bank can use its data across the organization.

Dinesh Kumar Nuthi is an Engagement Manager in Analytics & AI at Straive, specializing in fraud prevention, financial crime risk management, and digital transformation for leading U.S. financial institutions. With over 9 years of experience across the U.S., Canada, and India, he has led cross-functional teams to deliver analytical and digital solutions that enhance fraud detection, reduce losses, and drive operational efficiency. Dinesh has managed large-scale analytics programs involving analytics, machine learning, automation, and real-time risk monitoring. A data-driven leader, he has worked closely with senior stakeholders to align solutions with business strategy while mentoring global teams. He is currently pursuing a part-time MBA from Leeds School of Business and is passionate about using technology and analytics to solve high-impact business problems.